Most operators treat insurance as a legal checkbox. That is expensive.

If your branch team cannot explain what is covered, what is excluded, what must be documented, and what changes when a customer declines optional protection, your operation is carrying hidden risk even when a policy technically exists.

The real objective behind car rental insurance requirements is not paperwork. It is operational control: fewer avoidable disputes, faster claim resolution, cleaner customer communication, and better margin protection.

Insurance is an operating system, not a contract PDF

A policy document does not protect your margin by itself. Your workflow does.

In practice, insurance performance depends on whether five moments are controlled:

- Reservation disclosures

- Pickup verification and acceptance

- Vehicle condition evidence

- Incident response timing

- Claim file completeness

If any one of those breaks, your policy can still exist while your economics break.

A simple coverage architecture for rental operators

Most rental teams overcomplicate product names and under-define decisions. Keep the architecture simple:

Scroll to compare every column

| Layer | Operational purpose | Typical owner |

|---|---|---|

| Base liability coverage | Protects against third-party liability exposure | Company policy + legal/compliance lead |

| Vehicle damage handling model | Defines how physical damage is handled and recovered | Ops + finance |

| Customer protection options | Clarifies optional waivers/protection at booking and pickup | Sales/branch leaders |

| Deposit and authorization rules | Controls immediate financial exposure and behavior incentives | Finance + branch operations |

| Claim evidence protocol | Ensures recoverable incidents are documented correctly | Branch + back-office claims |

This model makes insurance discussion actionable for operators, not only for brokers.

The four failure modes that create claim chaos

When claims get expensive, root causes are usually operational, not actuarial.

1) Coverage terms are not translated into branch behavior

Teams know they are “insured,” but they do not know what events require immediate escalation, what documentation is mandatory, or how fast reports must be submitted.

2) Optional protection is explained inconsistently

If one agent frames protection as “recommended” and another as “almost mandatory,” dispute risk rises. Consistency matters for both conversion quality and legal defensibility.

3) Deposits are disconnected from risk level

A one-size-fits-all deposit policy creates avoidable loss on high-risk rentals and unnecessary friction on low-risk rentals.

4) Evidence is captured late or incompletely

If handoff photos, timestamps, IDs, and signed acceptance are fragmented across chats and devices, claims become slow and costly even when you were right.

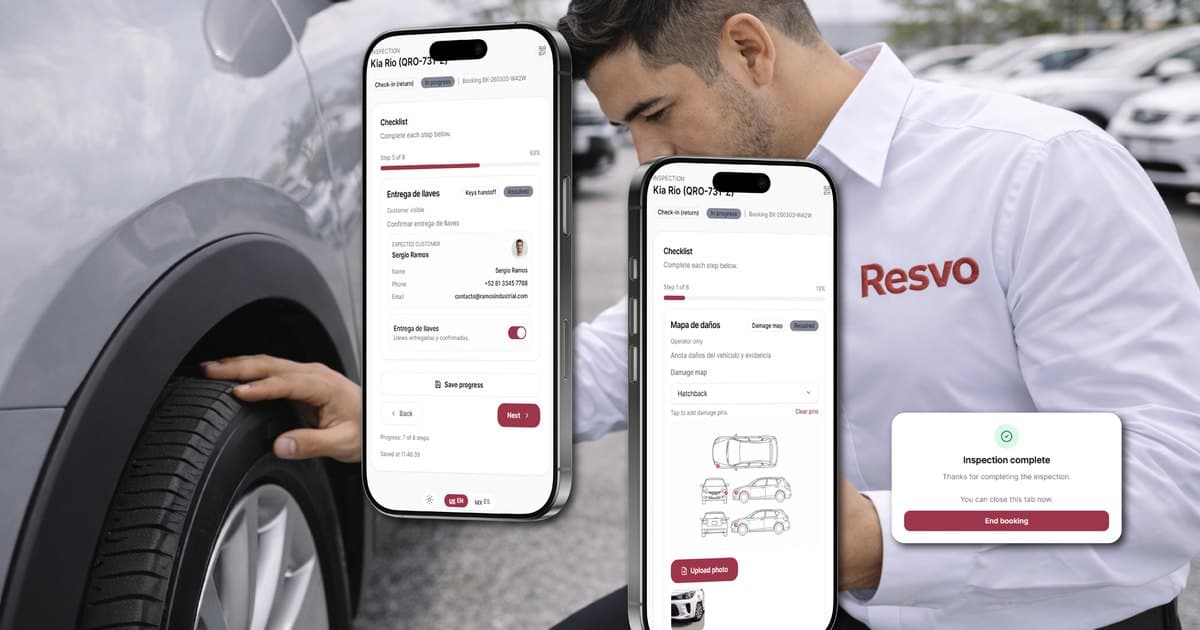

Build an insurance-ready handoff checklist

Your branch needs one repeatable checklist that runs every time.

Pre-pickup controls

- Confirm booking data and driver identity match

- Confirm selected protection option is clearly recorded

- Confirm deposit/authorization rule for that vehicle class

- Confirm customer sees key exclusions in plain language

Vehicle release controls

- Capture timestamped condition photos/video

- Capture signed acceptance of terms and condition state

- Record fuel/charge level and mileage

- Attach all records to the reservation, not personal devices

Incident controls

- Define a single escalation route and response target

- Capture scene evidence and customer statement quickly

- Lock all incident artifacts to one case record

- Trigger claim workflow with standardized required fields

This is where many operators recover margin: not by buying a more complex policy, but by running a clean protocol every time.

Segment your rules by risk context, not only by vehicle class

Vehicle class matters, but it is not enough. A compact sedan can carry very different risk depending on context.

Use a risk matrix that combines:

- Vehicle category

- Rental duration

- Driver profile and verification confidence

- Channel type (direct web, corporate, OTA, counter walk-in)

- Historical incident patterns

Then set deposit, documentation depth, and escalation thresholds accordingly.

Align insurance language with booking language

One of the biggest trust failures is mismatch between online promise and counter reality.

To prevent that:

- Use the same protection labels across booking, contract, and invoice

- Make exclusions visible before payment, not after handoff

- Keep short plain-language summaries for branch scripts

- Log customer acceptance in the reservation record

If you are still stabilizing booking quality, pair this with car rental software with online booking and car rental software vs spreadsheets.

KPI stack: how to know your insurance operations are healthy

Track insurance as an operating performance layer, not only as annual premium cost.

Scroll to compare every column

| KPI | Why it matters | Warning threshold |

|---|---|---|

| Incident-to-claim conversion time | Slow starts reduce claim recoverability | >24 hours average |

| Complete evidence rate at handoff | Predicts claim defensibility | <95% complete files |

| Deposit adequacy by risk band | Signals exposure mismatch | Frequent manual overrides |

| Dispute rate on protection charges | Reveals communication quality gaps | Rising month-over-month |

| Net loss per incident | True economic impact after recoveries | Trending upward over 2-3 cycles |

These indicators let you intervene before losses become “normal.”

Where Resvo fits

Resvo helps rental operators connect protection choices, deposits, contracts, identity checks, handoff evidence, and incident records in one operating flow.

That removes the common gap where insurance “exists,” but branch execution is fragmented.

If you are building a stronger risk stack, continue with KYC for car rental fraud prevention, car rental software with Stripe, and the full product workflow. When you want to map this to your current operation, book a demo.

Source references

- Insurance Information Institute: Rental car insurance

- National Association of Insurance Commissioners: Auto insurance overview